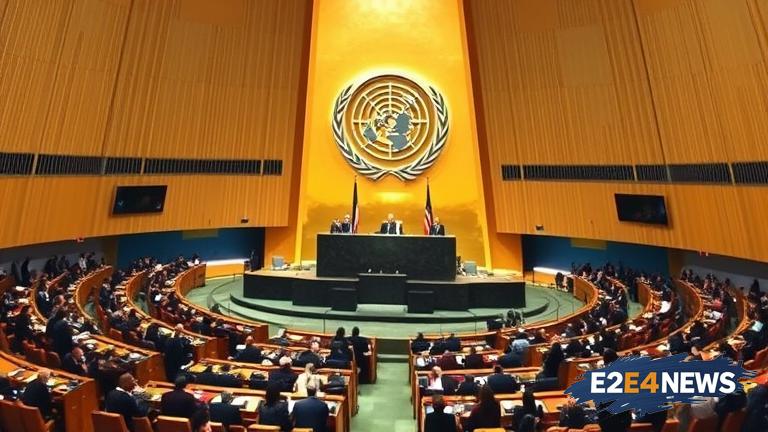

The United Nations General Assembly is currently deliberating on a proposal that could significantly impact the organization’s internal audit processes. The proposal, which has been put forth by the Assembly’s auditing committee, suggests separating the audit functions of the UN into distinct entities. This move is intended to bolster transparency and accountability within the organization, allowing for more effective oversight and management of its resources. The proposal has been met with a mix of reactions, with some member states expressing support for the initiative, while others have raised concerns about the potential implications. Proponents of the proposal argue that separating the audit functions would enable the UN to better identify and address instances of inefficiency, corruption, and mismanagement. They also contend that this move would help to enhance the credibility and trustworthiness of the organization, both among its member states and the global community at large. On the other hand, critics of the proposal have voiced concerns about the potential costs and logistical challenges associated with implementing such a change. They also argue that the current audit system, although imperfect, has undergone significant reforms in recent years and is capable of effectively serving the organization’s needs. Despite these concerns, the proposal has garnered significant attention and support from various stakeholders, including some member states and civil society organizations. The General Assembly is expected to continue debating the proposal in the coming weeks, with a vote on the matter potentially taking place in the near future. If approved, the separation of audit functions would mark a significant shift in the UN’s internal governance structure, with potential far-reaching implications for the organization’s operations and reputation. The proposal has also sparked discussions about the broader role of auditing and oversight within international organizations, highlighting the need for greater transparency and accountability in global governance. As the debate unfolds, it remains to be seen whether the General Assembly will ultimately decide to adopt the proposal, and what the consequences of such a decision might be. The UN’s auditing committee has emphasized the importance of careful consideration and thorough evaluation of the proposal, stressing that any changes to the audit system must be carefully planned and implemented to avoid disruptions to the organization’s operations. Meanwhile, some member states have begun to explore potential alternatives to the proposal, including reforms to the existing audit system that could achieve similar goals without requiring a full separation of functions. The General Assembly’s consideration of the proposal has also highlighted the need for greater cooperation and collaboration among member states, as well as between the UN and other international organizations. As the global community continues to grapple with complex challenges such as poverty, inequality, and climate change, the importance of effective and accountable global governance has become increasingly clear. The UN’s ability to adapt and evolve in response to these challenges will be crucial in the years ahead, and the outcome of the current debate on audit functions will be an important indicator of the organization’s commitment to transparency, accountability, and good governance. The proposal has also sparked interest among scholars and researchers, who are examining the potential implications of the proposed changes for the UN’s internal dynamics and external relationships. Some have argued that the separation of audit functions could have significant implications for the organization’s ability to respond to emerging global challenges, while others have suggested that the proposal could help to strengthen the UN’s role as a champion of transparency and accountability. As the debate continues, it is likely that a range of different perspectives and opinions will be heard, reflecting the diversity of views and interests among the UN’s member states and other stakeholders. Ultimately, the decision on whether to separate the UN’s audit functions will depend on a careful weighing of the potential benefits and drawbacks, as well as a thorough consideration of the organization’s overall goals and priorities. The General Assembly’s deliberations on the proposal are expected to be closely watched by observers around the world, who will be keen to see how the organization navigates this important issue and what the outcome might be. The proposal has also highlighted the importance of ongoing reform and improvement within the UN, as the organization seeks to adapt to changing global circumstances and to address the evolving needs and expectations of its member states. As the UN continues to evolve and grow, it is likely that further debates and discussions about its internal governance and operations will take place, reflecting the organization’s commitment to transparency, accountability, and good governance.

Mon. Sep 22nd, 2025

Trending

Bono’s Stance on Israel: Unpacking the U2 Frontman’s Views

Bono’s Stance on Israel: Unpacking the U2 Frontman’s Views

Israel’s Ongoing Occupation: Syrian Territory Remains Under Military Control

Israel’s Ongoing Occupation: Syrian Territory Remains Under Military Control

Rare Javan Leopard Rescued from Village Warehouse in Indonesia

Rare Javan Leopard Rescued from Village Warehouse in Indonesia

Telangana Leader Jagga Reddy Extends Generous Support to Ailing Girl

Telangana Leader Jagga Reddy Extends Generous Support to Ailing Girl

Empowering Young Minds: BGWC Mentorship Scholarships Guidance

Empowering Young Minds: BGWC Mentorship Scholarships Guidance